Introduction

The Ultimate beginner's guide to credit scores : Boost your financial future

If you’re starting out with personal finance, credit scores might seem tricky, but they don’t have to be. This beginner’s guide to credit scores will break down what a credit score is, why it matters in India, and how you can boost it to get better chances for loans, credit cards, and lower interest rates.

Whether you’re looking to buy a home, take out a personal loan, or apply for a credit card, your CIBIL score is a key factor that lenders use to judge your financial reliability.

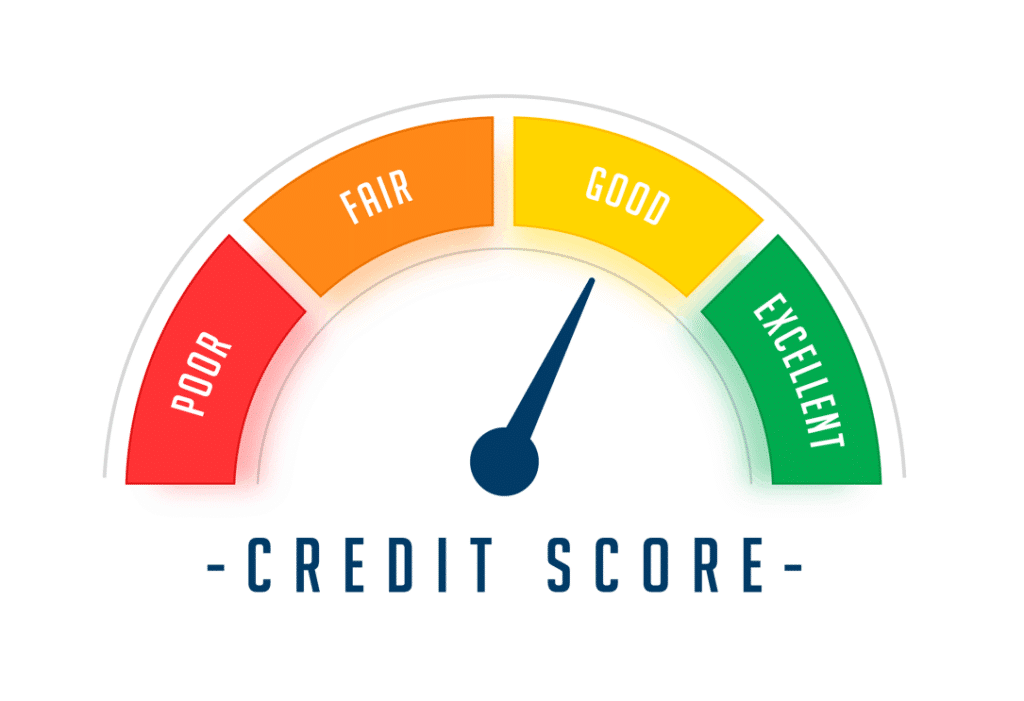

What Is a Credit Score?

If you’re new to credit and loans, understanding how credit scores work can feel confusing. Think of your credit score as a three-digit report card for your financial behaviour. In India, this score typically ranges from 300 to 900 and tells banks and NBFCs how responsible you are with borrowed money.

A higher score means lenders see you as low-risk and financially trustworthy, which increases your chances of getting loans approved faster and at better interest rates. As a beginner, learning how your credit score works is a powerful first step toward taking control of your money, avoiding loan rejection, and building a confident financial future

Credit Score Range in India

Score Range Meaning Impact on Loans & Cards

750–900 Excellent Easier approvals, lower interest rates

700–749 Good Loan approvals likely, moderate rates

650–699 Fair May face scrutiny, higher rates

600–649 Poor Difficult to obtain loans

<600 Very Poor High risk, loan denial likely

How Is a Credit Score Calculated in India?

Credit bureaus like CIBIL, Experian, Equifax, and CRIF High Mark primarily calculate credit scores in India. Several factors determine your score:

1. Payment History (35%)

Timely repayment of EMIs, credit cards, and loans.

2. Credit Utilization Ratio (30%)

Ratio of your outstanding credit to your credit limit. Could you keep it below 30%?

3. Credit Mix (10%)

A healthy mix of secured (home loan) and unsecured (credit card) loans improves your score.

4.Credit Age (15%)

The longer your credit history, the better your score.

5. New Credit Inquiries (10%)

Too many loan or card applications can lower your score.

Pro Tip: Maintaining a disciplined repayment habit and keeping your credit utilization low are two of the most effective ways to maintain a healthy credit score.

Why Credit Scores Are Important in India

Beginner’s Guide to Credit Scores influences multiple aspects of your financial life:

✅ Loan Approval: Banks use your score to decide whether to approve personal, home, or auto loans.

✅ Interest Rates: Higher credit scores can fetch lower interest rates, saving thousands of rupees over time.

✅ Credit Card Approvals: Even premium cards require a minimum credit score for eligibility.

✅ Rental and Employment Verification: Some landlords and employers check credit history for trustworthiness.

By understanding credit scores, beginners can make informed financial decisions, avoid unnecessary debt, and achieve long-term financial stability.

Beginner Tips to Improve Credit Score

Improving your credit score requires discipline and patience. Here’s a step-by-step approach suitable for beginner’s guide to credit scores:

1. Pay Your Bills on Time

Late payments on EMIs, credit cards, or utilities negatively impact your score. Set reminders or automate payments to ensure timely repayment.

2. Keep Credit Utilization Low

Maintain credit utilization below 30% of your total limit. High utilization signals risk to lenders and can lower your score. If your limit is ₹1,00,000 — try to use only ₹30,000 or less.

3. Avoid Multiple Credit Applications

Applying for too many loans or credit cards at once can reduce your score. Only apply when necessary.

4. Maintain a Healthy Credit Mix

A mix of secured and unsecured loans improves your credit profile. For example, a combination of a home loan and a personal loan demonstrates responsible borrowing behaviour.

5. Monitor Your Credit Report Regularly

Check your credit reports from CIBIL, Experian, or Equifax once or twice a year to correct errors and ensure accurate reporting.

Common Myths for Beginner's Guide to Credit Scores India

Myth 1: Checking your credit score lowers it.

✅ Fact: Checking your own score is a soft inquiry and does not impact it.

Myth 2: Having no debt is better for a credit score.

✅ Fact: No credit history may lead to a low score. Some responsible credit activity is beneficial.

Myth 3: Paying off one loan instantly improves your score.

✅ Fact: Credit scores update gradually, usually within 30–45 days after payments are reported.

Best Practices for Maintaining a Good Credit Score in India

✅ Always pay your credit card balance in full instead of just the minimum to avoid extra interest

✅ Pay off multiple credit cards strategically by focusing on higher-interest ones first or using a strategy that keeps you motivated.

✅ Keep your older credit accounts open, as they help boost your credit history.

✅ Maintain a healthy mix of loans—like personal, home, or education—to show responsible borrowing.

✅ Build an emergency savings fund so unexpected expenses don’t lead to late payments.

How Long Does It Take to Improve a Credit Score?

Improving your credit score is a gradual process. With consistent financial discipline, you can see noticeable improvement in 6–12 months.

Conclusion

Having a good credit score is key to staying financially healthy and opening doors to better opportunities. For beginners in India, learning how credit scores work, paying bills on time, keeping your credit usage low, and regularly checking your credit report are all steps toward building a strong credit profile. This beginner’s guide to credit scores will help you understand the essentials, make smarter financial choices, and gradually strengthen your credit—setting you on the path to long-term financial freedom. Start taking small steps today, and your future self will definitely thank you

FAQs

Q1. What is a good credit score for loans in India?

A score above 750 is usually considered very good. With this score, banks and lenders are more likely to approve your loans quickly and offer you lower interest rates.

Q2. How often should I check my credit score?

Checking your credit score every 3 to 6 months helps you correct any errors.

Q3. Does paying minimum balance improve credit score?

Maybe, but always try to pay your full dues to keep your credit score good.

Q4. Can I improve my score if I have no credit history?

Q5. How to correct errors in my credit report?

If you spot mistakes, submit a dispute through the official CIBIL website with the proper documents. The bureau will review and correct the errors.

Pingback: Powerful Tips on How to Pay Off Multiple Credit Cards Strategically

Pingback: Debt Consolidation Loan Guide: Powerful Tips to Choose the Best Option in India